At first glance, the chart below looks worrying. It shows a steady decline in the total number of small fleets — those with one to six trucks — across the U.S. throughout 2025.

From more than 183,000 early in the year to about 181,577 by fall, that’s roughly 1,500 small carriers exiting the market each month.

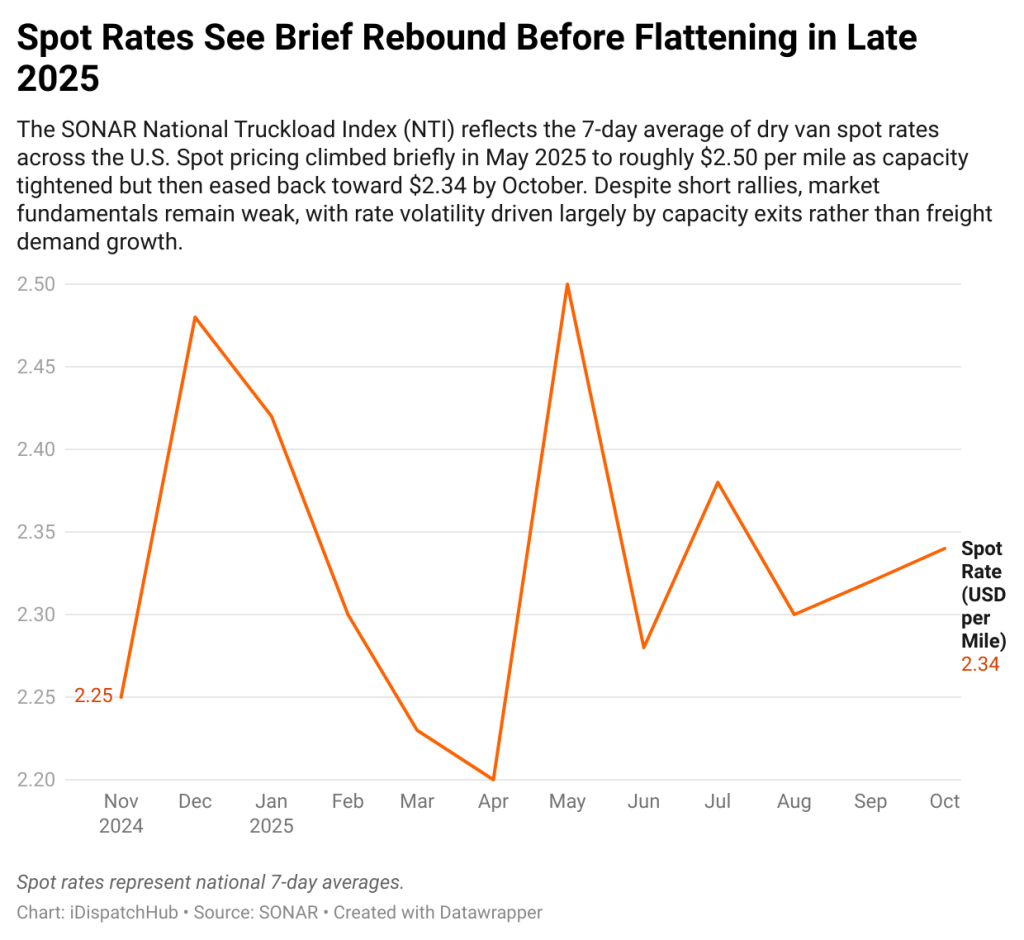

- This decline is a market correction, not an industry collapse, favoring prepared, business-minded carriers.

- Exits remove capacity, which can push spot rates up and improve negotiating power for survivors.

- Cost pressures—fuel volatility, flattened spot rates, and tighter regulation—forced many ill-prepared small fleets out.

- Remaining carriers and dispatchers gain value; disciplined operators can secure better broker relationships and higher margins.

If you’re a dispatcher or small-fleet owner, that headline might make your stomach tighten.

But before you panic, take a breath. This isn’t a death sentence for trucking — it’s a correction.

And for the right operators, it could actually be the best news in a long time.

The Reality Behind the Decline

What we’re seeing isn’t a collapse. It’s the result of market gravity finally catching up.

Over the past few years, we’ve lived through one of the biggest carrier booms in modern history. Between 2020 and 2022, sky-high spot rates and stimulus-driven freight demand pushed thousands of drivers to get their own authority. Everyone wanted in.

But like any gold rush, most came unprepared.

They weren’t ready for volatile fuel prices, low contract volumes, or the hard truth that trucking is a business — not a shortcut to independence.

Now, with freight rates normalizing and costs rising, the carriers who jumped in for quick wins are bowing out. What’s left are the ones who treat their trucks like assets, not lottery tickets.

What the Numbers Really Mean

This data chart shows small-fleet count hovering near 181,500 active authorities — down from the early-year highs near 184,000. That’s about a 1.3% decline in just ten months.

It might not sound like much, but every exit matters.

Here’s what that translates to on the ground:

- Fewer trucks chasing the same loads

- Less capacity on spot boards

- Better negotiating power for those still standing

If you’ve been struggling to find decent paying loads, that’s why things might slowly start to feel a little less desperate.

When capacity tightens, shippers and brokers can’t be as picky. They need reliable trucks. And they’re willing to pay more for consistency.

The Cost Pressures That Drove the Shakeout

Let’s be honest — this purge didn’t happen by accident.

Three main forces squeezed small fleets this year:

1. Fuel Prices Stayed Volatile

DOE diesel averages have bounced between $3.45 and $3.83 per gallon for twelve straight months. That’s the difference between profit and loss for a single-truck owner who budgets to the penny.

Many who entered the market during the low-cost pandemic years simply couldn’t handle $1,200-plus weekly fuel bills.

2. Spot Rates Flattened

The National Truckload Index sat near $2.35 per mile for most of the year — good by long-term standards, but a shock for anyone who built a business on $3.50 freight.

When rates normalized, the newcomers realized that success in trucking isn’t about finding “high paying loads.” It’s about controlling costs, managing relationships, and surviving through cycles.

3. Regulation and Compliance Tightened

FMCSA’s ELP (English Language Proficiency) enforcement, the crackdown on non-domiciled CDLs, and the ongoing fraud investigations around double brokering and MC swapping have all raised the bar.

Many small fleets couldn’t keep up with the paperwork, insurance renewals, or security deposits required to stay active.

So, they parked the trucks, closed the authorities, or went back to driving for someone else.

Why This Isn’t All Bad News

The freight market has always been cyclical. Carriers come and go — but each wave of exits strengthens the next one of survivors.

Here’s why this downsizing could actually help serious operators:

1. Less Capacity = Stronger Rates

Every fleet that exits removes trucks from the marketplace.

That tightening supply eventually pushes rates upward, especially as we move into seasonal surges like holiday freight and Q1 replenishment.

If you’re still in business right now, you’re positioned perfectly to benefit from that coming shift.

2. Fewer Fly-By-Night Competitors

During the 2021–2022 boom, the industry was flooded with first-time carriers — some running under shady dispatch setups or fake MC numbers. They undercut rates, ran unsafe, and hurt the reputation of small trucking.

Now, with FMCSA cleaning up the data and stricter insurance oversight, those same operators are vanishing.

The ones left — the disciplined, compliant, relationship-driven fleets — are finally getting the breathing room they deserve.

3. Better Broker and Shipper Relationships

When capacity tightens, brokers value consistency. They remember the carriers who delivered through chaos.

Small fleets that stayed professional through low-rate seasons are now the first ones brokers call when volumes rebound.

If you’ve been playing the long game — communicating, updating, showing up on time — that investment is about to pay off.

4. Opportunities for Dispatchers

Here’s where it gets interesting for dispatchers.

As small-fleet counts shrink, each remaining carrier becomes more valuable. If you can help them stay efficient — cutting deadhead, managing detention, watching fuel, and keeping their books in order — you’re not just a dispatcher anymore.

You’re an operations partner.

And that’s where the next generation of dispatch services will grow — from simple load booking to full business support.

A Note on Market Cycles

Let’s zoom out.

What we’re witnessing is a natural rebalancing. Trucking expands when freight is easy, then contracts when it isn’t.

The real professionals — those who understand cash flow, compliance, and market timing — use contractions to reposition.

They renegotiate fuel cards. They clean up debt. They trim weak lanes and focus on profitability instead of volume.

Because when the next freight wave hits (and it always does), they’ll have less competition and stronger footing.

What Dispatchers Should Be Watching Next

If you’re dispatching for carriers right now, here’s what to keep your eyes on:

- FMCSA Enforcement Trends:

As the ELP program fully rolls out, expect more shutdowns of unqualified operators. That’ll further reduce capacity in 2026. - Fuel Stability:

DOE diesel prices hovering around $3.75 are sustainable — but any surge past $4.00 could trigger another round of exits. - Spot Rate Recovery:

With small-fleet counts declining, we could see a rate rebound in early 2026, especially in reefer and flatbed markets that already show tightening rejection rates. - New Entrant Data:

Watch for whether new MC registrations pick back up. If not, expect leverage to stay with carriers well into Q2.

For New Entrants — Don’t Let This Scare You

If you’re a driver thinking about starting your own authority right now, don’t take this as a warning to stay away. Take it as a call to prepare better.

Because this new environment — leaner, regulated, and disciplined — rewards business-minded owners.

Get your books right.

Find a solid dispatcher.

Build direct shipper relationships.

Stay compliant.

You don’t have to compete with 200,000 other small carriers anymore — only the serious ones.

That’s not bad news. That’s a fresh start.

The Bottom Line

Yes — small fleets are shrinking.

Yes — it’s tough out there.

But no — it’s not the end of small trucking.

This is the cleanup phase that happens before every recovery. The same thing happened after 2019’s bloodbath and after 2008’s crash.

The strong adapt, the unprepared exit, and the cycle resets.

For dispatchers and carriers who are still standing — this is your moment to get lean, get smart, and get ready.

Because fewer trucks on the road don’t just mean fewer competitors. It means more opportunity — if you know how to seize it.