2026 won’t be a repeat of 2020, 2021, or 2023. It won’t look like the post-pandemic bull run, and it won’t look like the long, grinding downturn that followed. What we’re heading into is an entirely different kind of cycle—one shaped by structural attrition, regulatory tightening, consumer recalibration, inflation that refuses to fully cool, and a freight network that spent three years resetting its own expectations.

- Demand edges up modestly as consumers stabilize, yielding steady but uneven freight growth across sectors.

- Capacity continues to shrink—small-fleet exits, tougher financing, and regulatory enforcement tighten available trucks.

- Rates firm with 5–12% upside; spot market moves sideways with upward bias as costs and compliance raise floors.

- Technology and disciplined operations separate winners—AI, efficiency, and compliance drive profitability in 2026.

To understand 2026, you can’t look at a single chart. You have to merge multiple research lenses: tender data, housing starts, manufacturing sentiment, diesel futures, monetary policy trajectory, Class-8 order behavior, regulatory enforcement trends, and driver demographics. Only then does the picture become clear: 2026 is shaping up to be a “pressure-point” year—a year where small shifts in supply and demand can cause outsized rate responses.

Let’s break down the forces shaping the year ahead.

The Demand Side: The Freight Economy Rebuilds, Slowly but Deliberately

Consumer Spending

The American consumer—the true engine of trucking—walks into 2026 more stable than in 2023–2024, but not in full expansion mode. Retail inventories have recalibrated, e-commerce is still growing high-single digits annually, and household balance sheets are healthier than expected. But consumers are also more price-sensitive than they were during stimulus years. That creates steady, but not explosive, goods movement.

Freight demand grows when consumers shift from services back to goods. Early signals suggest a modest rebalancing in 2026 due to:

- Slower inflation

- Soft landing conditions

- Lower real interest rate pressure

- A slight return to durable goods purchases

This points to a 2–3% increase in total freight demand, spread unevenly across sectors.

Housing and Construction

Housing is historically one of trucking’s strongest predictors. With mortgage rates finally stabilizing and backlog clearing, 2026 sets the stage for:

- More construction freight

- More flatbed opportunities

- Increased regional building materials demand

Not a boom, but a climb from the lows of the prior cycle.

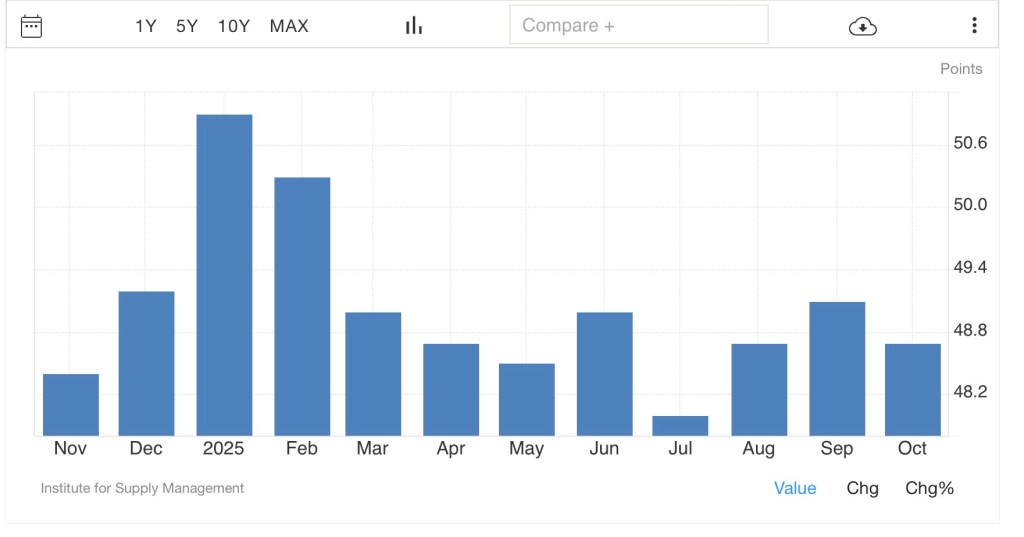

Manufacturing and Industrial Production

ISM Manufacturing had been stuck in contraction for an extended period, but forward indicators show slow improvement into late 2025 and early 2026. Manufacturing isn’t roaring back, but the bottom appears to be behind us, creating a foundation for incremental freight expansion.

The Supply Side: Capacity Will Keep Falling Into 2026

Authority Revocations

The last three years were brutal for small carriers. High fuel prices, collapsing spot rates, insurance increases, and weak operating discipline flushed thousands out of the market. That trend is still underway.

Expect at least another 3–5% reduction in active small-fleet capacity through mid-2026 based on:

- Rising insurance premiums

- Aging equipment fleets

- Tougher financing

- A shrinking pool of viable owner-operators

- Non-domiciled CDL scrutiny removing drivers

- ELP enforcement restricting borderline operators

This reduction doesn’t happen in a single spike—it happens drip-by-drip, week-by-week, exactly the way structural tightening typically unfolds.

Class-8 Orders

New truck orders have cooled significantly. Fleets aren’t expanding—they’re refreshing. Replacement cycles remain steady, but growth cycles remain absent. This means capacity stays disciplined, preventing an overshoot like 2019.

Maintenance Costs

Parts costs have stabilized but remain high compared to pre-pandemic. Aging trucks cost more to run, pushing weak operators out and strengthening the position of professionally run fleets.

Regulatory Pressure: The Silent Force That Will Reshape 2026

This is the most misunderstood freight influencer of all.

Non-Domiciled CDL Enforcement

Recent court interventions slowed parts of DOT’s crackdown, but scrutiny is not going away. California faces massive pressure to revoke improperly issued licenses. Other states will follow. This means thousands of drivers may be sidelined, directly altering capacity.

ELP Enforcement

The enforcement posture is tightening. CVSA wants a clearer, more aggressive strategy. FMCSA is under political pressure to clean up the industry after multiple high-profile incidents.

Compliance will act as a “stealth capacity reducer.”

ELDT Audits

Entry-Level Driver Training compliance audits are increasing. Training gaps—especially in carriers with high turnover—will trigger more interventions and more OOS risk.

Broker Compliance

The new Broker Financial Responsibility Rule places pressure on brokers to operate cleanly or face suspension. This creates a cleaner market and forces dispatchers and carriers to engage with more reliable intermediaries, reducing fraud-related disruptions.

The theme across all regulation: higher scrutiny = lower capacity. And lower capacity = upward rate pressure.

Freight Rates: The 2026 Rate Environment Will Look Nothing Like 2020–2022

The days of $3.50–$4.00/mile van freight aren’t returning in 2026—not without an external shock. But the days of $1.60 freight are ending too. Rates will rise for one reason: capacity attrition outpaces demand growth.

Expect:

- 5–12% rate increases across dry van and reefer

- More pronounced increases regionally (Upper Midwest, Southeast, Mountain regions)

- Flatbed volatility tied to construction cycles

- Stronger rate floors due to insurance, diesel, and compliance costs

The spot market will feel different: not volatile up and down—volatile sideways with upward bias. This is the kind of market where dispatchers who understand timing, lanes, and net revenue per day will outperform averages consistently.

Fuel Markets: Diesel Will Become a Deciding Factor Again

Diesel sits in a delicate position going into 2026.

Key factors:

- Geopolitical tension affecting crude

- Refining capacity constraints

- Seasonal diesel/heating oil overlap

- Domestic shale production leveling off

- Markets expect diesel to stabilize between $3.50–$4.10, with occasional spikes. Fuel will not collapse the way many carriers hope. It will remain a cost pressure.

Because diesel is steady but not cheap, it reinforces one reality: Efficiency will separate profitable carriers from the ones that barely hang on. Station selection and driving behavior remain the two controllable variables. Carriers who manage both will outperform peers by hundreds weekly.

Payroll, Drivers, and Labor

2026 introduces a new friction: labor costs rising faster than freight rates.

Drivers want:

- Higher pay

- Predictable home time

- Cleaner equipment

- Better dispatching

- More transparency

Professional fleets will adapt. Marginal operators will fail.

A quiet trend: more company drivers abandoning owner-operator dreams due to cost burden. This brings stability to larger fleets and instability to micro fleets.

Shipper Behavior: The Return of Rational Contracting

Shippers in 2026 will not chase the lowest rates like in the downturn. They’ve learned two painful lessons:

- Cheap carriers collapse

- Compliance problems cost more than rate increases

- Broker fraud and cargo theft risk rise when vetting fails

Shippers will prioritize:

- Reliability

- Compliance

- On-time metrics

- Shipment visibility

This creates an opportunity for small, clean fleets to win more freight—even at slightly higher rates.

Broker Behavior: More Cautious, More Data-Driven

Brokers will be squeezed between new regulations and shrinking carrier capacity.

Expect:

- Stricter vetting

- More focus on carrier performance

- Higher value placed on reliability and communication

- Less tolerance for unprofessional dispatching

This benefits carriers and dispatchers who operate with discipline and documentation.

Technology, Automation, and AI: The Next Efficiency Wave

2026 will be the year AI stops being cool and starts being mandatory.

Key changes:

- AI predictive pricing becomes standard

- Freight matching becomes more automated

- Carrier selection algorithms prioritize compliance

- Dispatchers who rely solely on load boards lose competitive footing

- Small carriers begin adopting automated back-office systems

Technology won’t replace dispatchers, but it will expose weak ones.

The winners will use technology as a multiplier—not a crutch.

The “Tightening Spiral”: Why 2026 Will Feel Better Than 2025

2026 is not a boom year. It is a tightening year.

Here’s the math:

- Freight demand rises modestly

- Capacity drops meaningfully

- Regulation removes marginal operators

- Operating costs rise

- Shippers prioritize reliability over cost

That combination always produces rate stabilization with upward bias.

The first half of 2026 is still transition.

The second half is where pressure builds and rate power quietly shifts back to carriers.

Risks Worth Watching

No forecast is complete without identifying threats:

Downside risks:

- A consumer slowdown

- A crude price spike above $100

- Sudden shocks to manufacturing

- Geopolitical disruption

- Unexpected regulatory shifts

Upside risks:

- Faster-than-expected housing recovery

- Accelerated small-fleet exits

- Stronger retail demand

- Favorable diesel price stabilization

- Higher OTRI in reefer leading to spot market tightening

Final Outlook for 2026

2026 won’t reward the loudest carriers or the luckiest dispatchers. It will reward the most prepared.

Expect:

- A steady climb in rates

- A meaningful reduction in capacity

- A stricter regulatory landscape

- A consumer-driven but moderate demand recovery

- Stronger carrier leverage in the back half of the year

- Technology-driven efficiency gains

- A widening gap between professional operations and everyone else

This is a year built for disciplined carriers, structured dispatchers, and business owners who track their numbers. Those who manage fuel, negotiate with strategy, measure net revenue per day, and maintain compliance will win.

Everyone else will feel squeezed.

2026 won’t be the year the market explodes.

It will be the year the market reshapes itself—and rewards the people who respected the cycle even when it was painful.

If you understand that now, you’ll be miles ahead when the rest of the industry realizes the cycle has already turned.